Andrew Barr/National Post Near the end of her working life, Lise gets help to raise returns from her investments and calculate cash flow.

Situation: Near the end of her working life, a Quebec teacher wants to raise her retirement income

Solution: Use cash on hand to clear mortgage, then raise returns from investments, calculate cash flow

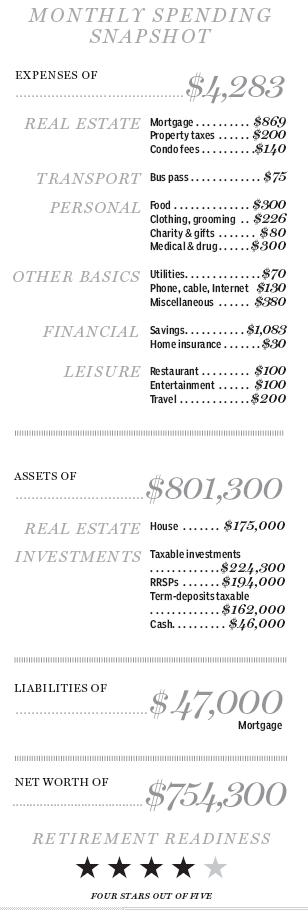

Lise, 65, as we’ll call her, teaches art at an elementary school in Quebec. Single, she is her sole means of support. In her four decades of work she has built up savings and investments of $626,300. Her only debt is a $47,000 mortgage on her $175,000 condo. The mortgage has nearly eight years to run before it is paid off. That will be well into a retirement she hopes can begin in mid-2016. The question is: Can her savings and a teacher’s pension of $25,700 a year, Quebec Pension Plan benefits and Old Age Security support her?

“My goal is to visit my family in Europe as often as my finances permit,” Lise says. “But are my investments to supplement my pensions well-placed? I want to have $35,000 a year to spend.”

Family Finance asked Benoît Poliquin, lead portfolio manager of Exponent Investment Management Inc. in Ottawa, to work with Lise. In his view, her zeal to save will ensure that she is solvent in future.

Current finances

Lise’s defined-benefit pension will provide $2,142 a month before tax, which is about 30% of her present monthly $7,157 paycheque. Other sources have to add income so that she can cover allocations other than $1,083 savings a month at present. With a reorganization of her balance sheet, all that can happen, Mr. Poliquin suggests.

Her monthly after-tax income, which includes her salary and her Quebec Pension Plan benefits, which she is already receiving, adds up to $4,283, the planner notes. Her $47,000 outstanding balance on her mortgage is a problem, for retired persons should be debt-free.

Lise has $46,000 in cash earning almost nothing that can be used to pay off the mortgage, which will have several thousand dollars less owing when it comes up for renewal in 2016, about the time she will be retiring. The remaining problem is to increase her cash flow for travel and other things she has put off for many years — clothing, dining out and the other pleasures of life. That can be done by adjusting her investments.

Lise’s monthly pensions will include $907 from the Quebec Pension Plan, which she already receives, $564 from Old Age Security, $2,142 from her teacher’s pension, $747 from taxable investment income and $742 accumulating in her RRSP. It adds up to $5,102 before tax and about $3,400 after tax on all income other than that held in RRSP. That’s an annual after-tax income of $40,800 and more than Lise’s $35,000 annual retirement income goal. With her mortgage paid off, her discretionary income will rise. Yet for more European travel, she will need higher income.

Raising returns

Her assets both registered and unregistered are in a buffet of bank-sponsored mutual funds. Her portfolio of term deposits is in taxable accounts. This is backwards, Mr. Poliquin says. Interest-bearing deposits such as bonds and bank deposits should be in registered accounts that have no current tax exposure because they are fully taxed as income. Her dividend-paying investments should be in taxable accounts in order to make use of the dividend tax credit and the tax reduction it provides. She has no Tax-Free Savings Account. Her TFSA space in 2014 is $31,000 and she can use it to shelter income from $432,300 she holds in taxable accounts. She can add money from $162,000 of maturing term deposits rather than transferring taxable investments to the TFSA. If she did the latter, the in-kind transfer would trigger tax on accrued but unrealized gains, the planner notes.

There is also a problem of asset allocation. It is haphazard, that is, whatever goes with the mutual funds she has chosen. Not only is the allocation unfocused, it does not relate to her risk tolerance and the potential swings on portfolio value that go with capital markets, Mr. Poliquin says.

At present, most of Lise’s retirement income will be government and teacher’s pensions, all of which are indexed. Value will not fluctuate with interest rates, but in every other sense, this income is as solid as government bonds. In her investment portfolio, she has a major fund company’s balanced fund with about 35% bonds and another company’s balanced fund with a similar bond weighting. Add it up and about 80% of Lise’s assets and income are from bonds.

Bonds used to pay interest well above what corporate stock dividends yield, but no more. Stock dividends, though less secure than interest on investment grade corporate bonds and government bonds, tend to be much higher than bond interest. Chartered banks pay 3.5% to 4.5% dividends on their common shares, worth about a quarter more after application of the dividend tax credit, while banks’ bonds pay about 1.5% to 3.5% depending on the bonds’ terms and seniority. The same relationships exist for large-cap telecom stocks, pipelines and mature industrial company stocks, Mr. Poliquin says.

Moreover, dividends have a tendency to increase over time at a rate that usually matches or surpasses inflation. The downside of using dividends for income is that the underlying shares can fluctuate in price dramatically.

If the portfolio was adjusted to reduce bonds to one-third and dividend-paying stocks to two-thirds, then Lise’s $626,300 portfolio could generate about 2% more income. That’s about $12,500.

Lise is paying about 2.1% in management fees on her $418,300 of financial assets other than cash and GICs. That works out to $8,784 a year. She could save roughly half of that, about $4,400 a year, by using an independent portfolio manager who would charge just 1% of funds under management, Mr. Poliquin notes.

Adding up extra investment income and fees she can keep, Lise could have $16,900 more pre-tax investment income for travel or anything else she wishes. Add in the savings-ending mortgage payments, $10,428 a year.

There is a barrier to remodeling Lise’s portfolio, namely her apprehension about what can go wrong. That in turn is a question of balance. Holding a high cash position of about a third of the total portfolio amounts to averaging out the risk of loss from the present to the indefinite future via inflation eroding her purchasing power.

The portfolio remodeling will raise income and perhaps Lise’s retirement horizons. She will have no more risk, but about 40% more income. “The reward for taking the steps to review the portfolio and raise income is huge,” Mr. Poliquin says. “More income will support more time in Europe where she likes to holiday with her family. More income in Canadian dollars will compensate for future decline of the loonie against the Euro.”

There is a backstop to the plan — Lise’s innate frugalness. “It is likely that she will save a good deal of any increased income she achieves through portfolio reorganization,” Mr. Poliquin says. “In the end, it is her nature that will keep her financially secure.”

Click Here to See the Original Article