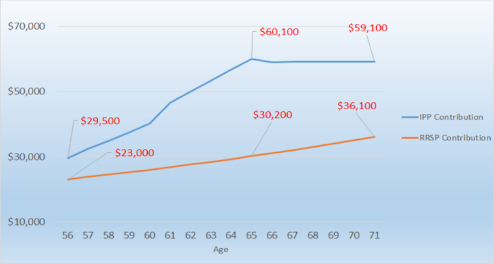

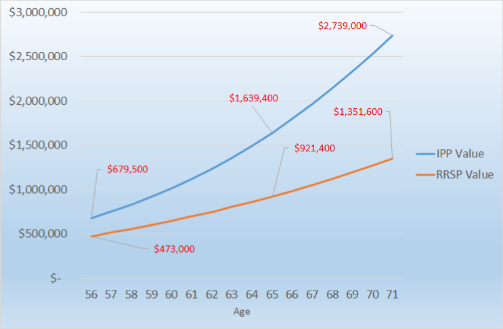

An IPP is a defined benefit plan which is exactly like the plans you would be a member of if you worked for large employers such as railway companies or the federal public service. In the case of the IPP, your company is the sponsor of the plan. IPPs are specifically designed for business owners. Your RRSP would be considered a defined contribution plan. The difference between a defined contribution (where you don’t know the outcome, but know how much you can contribute every year) and the defined benefit (where your contribution will be based on your age, years of service and salary and the retirement benefit is known) is the fact that the investment risk is borne by the contributor in the case of a defined contribution plan and the risk is borne by the sponsor in the case of a defined benefit plan.