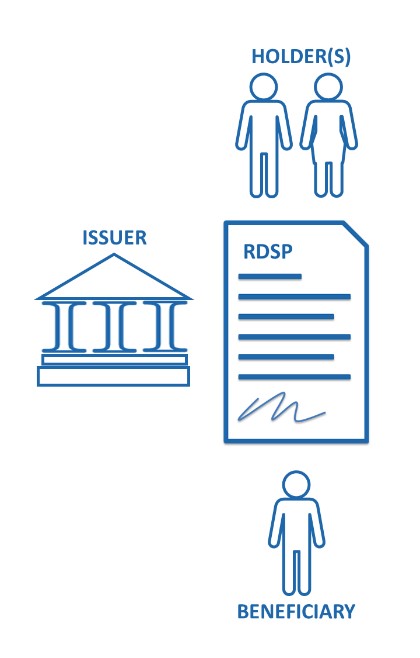

Registered Disability Savings Plans (RDSP) technically have three parties to the plan and each have their own eligibility requirements.

There are three parties to an RDSP:

- Holder(s): The person(s) who opens the plan, contributes, authorizes contributions and manages the plan.

- Beneficiary: The disabled individual who receives funds from the RDSP in the future.

- Issuer: The financial institution offering the RDSP.

The beneficiary of the RDSP must:

- Be eligible for the Disability Tax Credit (DTC)

- Have a valid Social Insurance Number (SIN)

- Be a Canadian resident when the plan is opened

- Be under the age of if 60, unless the RDSP is be opened as part of transfer from an existing RDSP

The beneficiary may also be the holder.

All holders must:

- Have a valid SIN or Business Number (BN) if an organization

Holders do not need to be a resident of Canada.

The beneficiary and the issuer are fairly straight forward concepts. The holder(s) are far more complicated to determine.

There are two main factors in determining who can be the holder(s) of an Registered Disability Savings Plan (RDSP):

- Beneficiary age

- Contractual competency

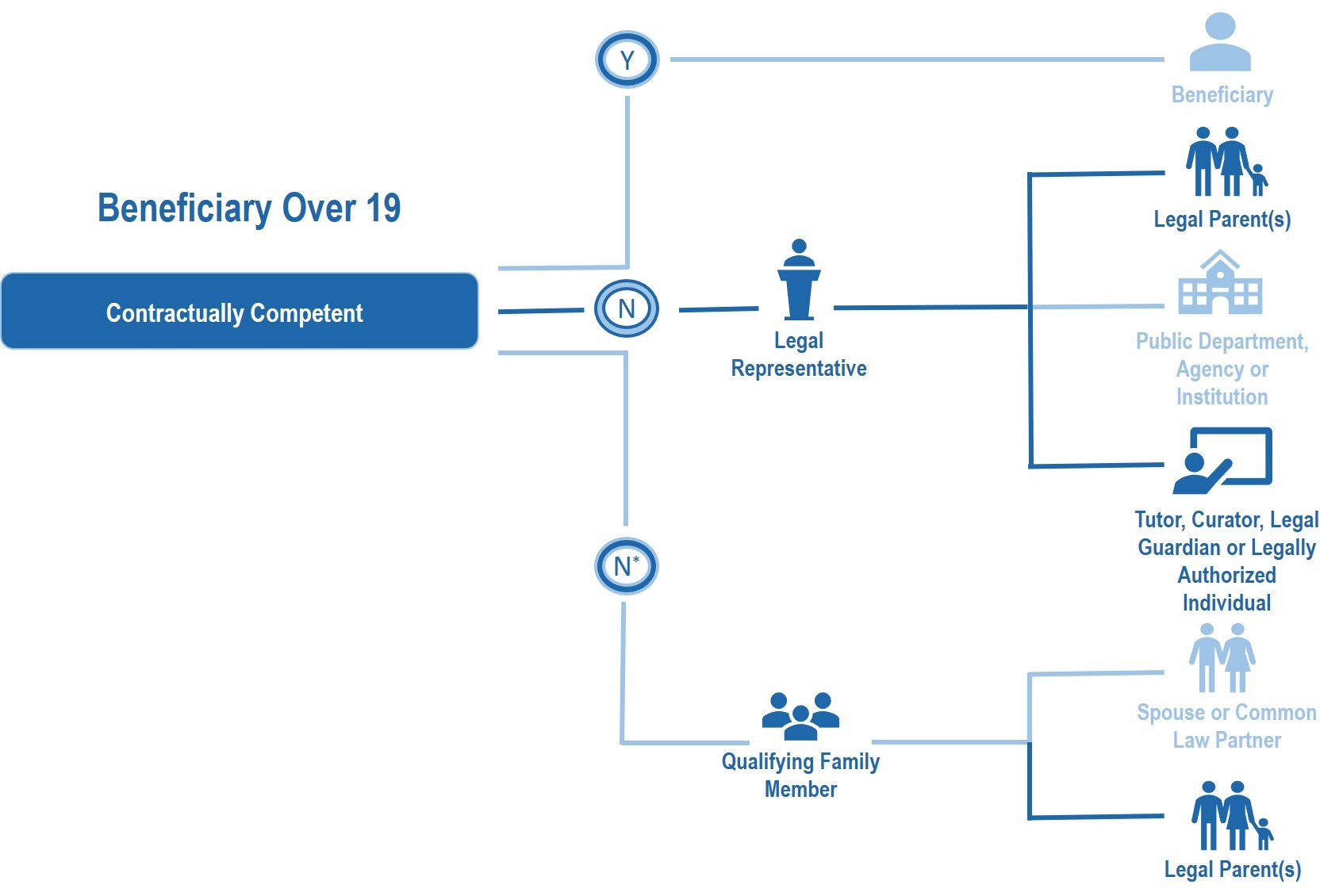

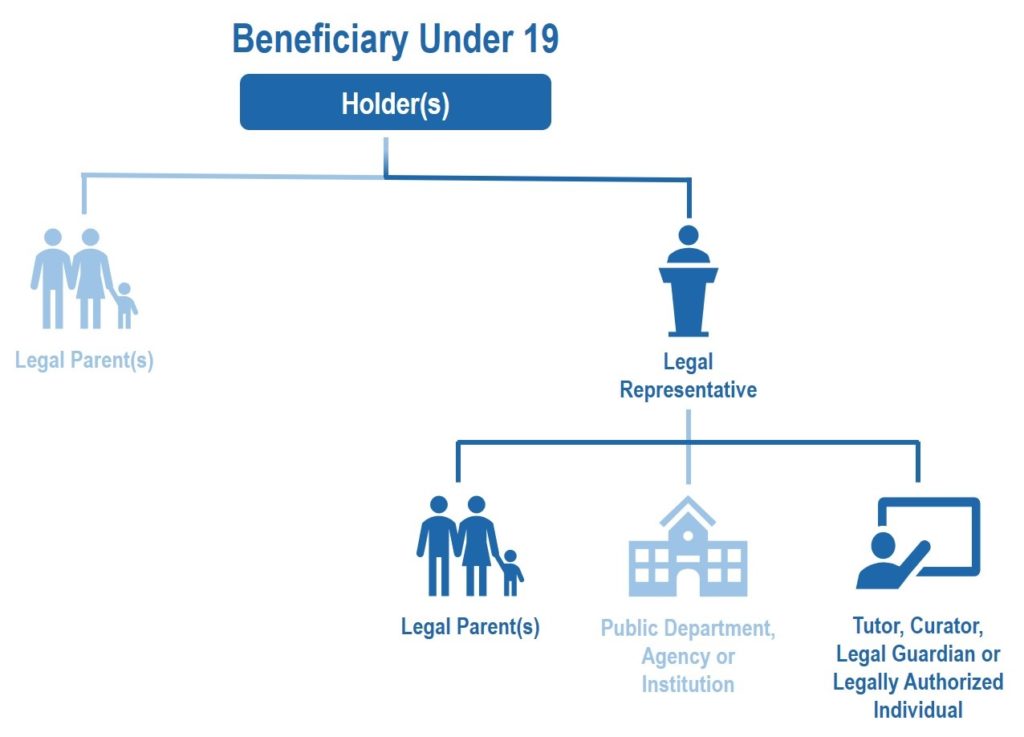

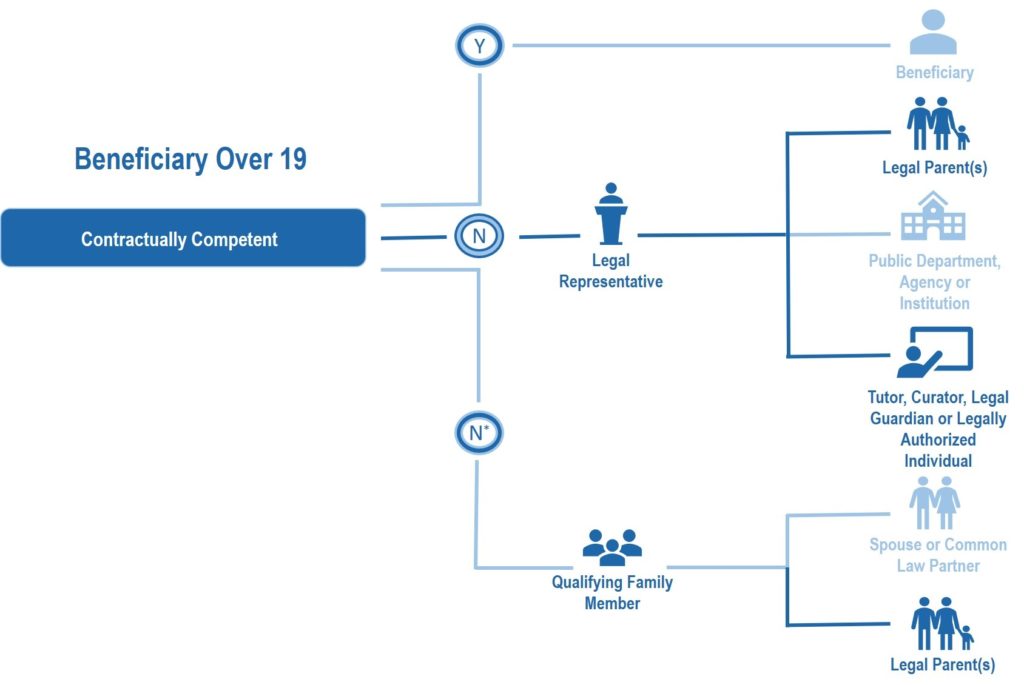

At age 19 the beneficiary must be added as a holder, if contractually competent. If the Registered Disability Savings Plan (RDSP) existed prior to beneficiary reaching age of majority, then a legal parent may remain as joint holder with the beneficiary.

At age 19 the beneficiary must be added as a holder, if contractually competent. If the Registered Disability Savings Plan (RDSP) existed prior to beneficiary reaching age of majority, then a legal parent may remain as joint holder with the beneficiary.

The N* in the diagram below addresses the situation where the beneficiary is not legally unable to contract, but mental competency is in doubt.

The 2012 Budget established a temporary measure that allows a Qualified Family Member (QFM) to be the holder for an adult beneficiary who may not be contractually competent.

Under this measure, financial institutions (issuers) may require a letter signed by a relevant medical practitioner stating that the beneficiary is not contractually competent.

The temporary measure expires December 31, 2018. After that date an RDSP may only be opened by QFM holders as part of the transfer of an existing plan between issuers, assuming the holders were acting in the same capacity on the existing RDSP.

The holder(s) of an Registered Disability Savings Plan (RDSP) can change over the lifetime of the plan.

The holder(s) of an Registered Disability Savings Plan (RDSP) can change over the lifetime of the plan.

It is important to note that it is the holder(s) who apply for the Canada Disability Savings Grant (CDSG) and the Canada Disability Savings Bond (CDSB).

Each time there is a change in holder(s), a new grant/bond application must be completed to continue receiving CDSG and CDSB.